Home Warranty vs. Homeowners Insurance: Climate Damage Coverage

Many homeowners struggle to distinguish between home warranty and homeowners insurance coverage, particularly for climate-related issues. The boundaries blur during events like floods, storms, or extreme temperatures. A clear comparison demonstrates that these protections address distinct financial and operational needs. Knowledge of these differences enables informed decisions that align cost management with practical expectations.

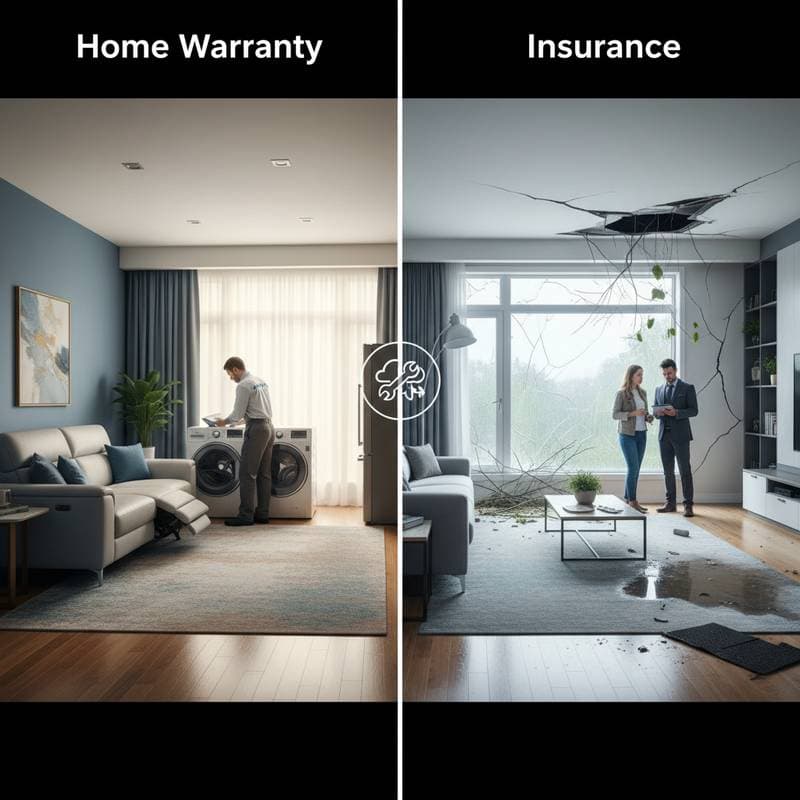

Defining Coverage Boundaries

A home warranty serves as a service contract focused on mechanical breakdowns in household systems and appliances. It targets issues from normal wear and tear, not external events. Coverage typically includes HVAC systems, water heaters, and refrigerators.

Homeowners insurance, however, safeguards against structural damage and loss of personal property from sudden occurrences. It addresses perils such as fires, windstorms, and specific water damage. Insurance handles external impacts, whereas warranties manage internal malfunctions.

Each option supports risk mitigation through separate mechanisms. Insurance operates as a regulated product that reimburses major losses. A warranty acts as a maintenance plan for repairs or replacements of specified items.

Cost Structure Analysis

The expense models for these protections vary significantly. Homeowners insurance premiums reflect factors like property value, location, and hazard levels. Areas prone to severe weather command higher rates. Deductibles range from several hundred to thousands of dollars, based on claim category and policy terms.

Home warranties follow a subscription approach. Homeowners pay a monthly or annual premium plus a service fee per technician visit. Service fees generally range from $75 to $150, with annual plans scaling by coverage scope.

The table below compares standard plans:

| Coverage Level | Monthly Cost | Service Fee | Coverage Limits | Key Exclusions |

|---|---|---|---|---|

| Basic Plan | $45 to $60 | $75 | Up to $2,000 per item | Pre-existing conditions, improper installation |

| Premium Plan | $65 to $90 | $100 | Up to $5,000 per item | Structural damage, natural disasters |

This overview indicates that warranties manage routine repair costs, while insurance covers substantial, unforeseen expenses.

Understanding the Claim Process

The homeowners insurance claim starts with reporting the damage. An adjuster evaluates the site to confirm the cause and policy applicability. Reimbursement occurs after approval, subject to exclusions and depreciation adjustments.

A home warranty claim proceeds as follows:

- Homeowner submits a service request to the provider.

- Provider dispatches a contractor for diagnosis.

- Provider assesses if the failure stems from normal wear, excluding misuse or external causes.

- Provider authorizes repairs or replacements within limits.

- Homeowner maintains records of routine upkeep to support ongoing claims.

Warranties emphasize adherence to maintenance protocols, in contrast to insurance focus on event documentation and loss assessment.

Coverage Limitations and Climate Damage Exceptions

Homeowners often expect comprehensive protection from both options against climate events, leading to unexpected costs.

Home warranties generally exclude natural disasters, severe weather, or flooding impacts. A lightning strike damaging an air conditioner compressor, for instance, falls outside coverage. Warranties apply only to inherent mechanical issues.

Homeowners insurance may cover certain weather events, yet exclusions persist. Standard policies omit floods, earthquakes, and progressive wear. Coverage for wind-driven rain requires roof breach from a covered storm; ground-level water entry remains uncovered without add-ons.

Such gaps necessitate multiple layers of protection. Residents in flood zones benefit from combining base insurance with flood endorsements, alongside warranties for non-weather appliance fixes.

Financial Implications of Climate Exposure

Climate vulnerabilities alter the value proposition for both protections. Rising weather threats elevate insurance premiums. Wind or hail deductibles might equal a percentage of dwelling value, amplifying out-of-pocket costs.

Home warranties show less direct climate influence, though environmental factors like humidity or thermal fluctuations accelerate breakdowns. Frequent claims can exhaust annual caps, shifting remaining expenses to homeowners.

To evaluate options, homeowners tally combined premiums, fees, and likely service calls against self-funding estimates. Households with modern equipment might find dedicated savings accounts more cost-effective than warranties.

Evaluating Provider Transparency

Both warranty and insurance agreements demand thorough review. Overlooked terms often restrict coverage during critical moments.

Home warranty policies commonly reject claims for inadequate maintenance or prior defects. Documentation of services, such as annual HVAC checks, proves essential.

Insurance terms may apply depreciation to reduce payments or deny secondary damages from late notifications.

Obtain a full sample contract before commitment, beyond promotional materials. Examine how providers handle sample claims involving vague language. Reputable companies disclose coverage caps, denial rates, and resolution paths. Opacity signals potential issues.

Decision Framework for Homeowners

A step-by-step approach separates hype from practical needs in selecting protections.

Step 1: Assess property risks. Map vulnerabilities to floods, high winds, or heat waves based on local patterns.

Step 2: Catalog home systems. Document appliances and systems, noting age, state, and repair estimates.

Step 3: Gauge financial capacity. Review emergency funds and tolerance for uncovered repairs.

Step 4: Map coverage intersections. Pinpoint redundancies that inflate costs or voids that expose risks.

Step 5: Vet provider reliability. Consult agency complaints and review sites for performance insights.

This method aligns choices with budget realities over sales pitches.

Building Comprehensive Home Protection

Complete defense against climate threats requires no isolated solution. Integrate insurance for major incidents, warranties for daily operations, and proactive upkeep for longevity.

Homeowners who scrutinize terms and costs achieve more than reassurance. They secure tangible fiscal resilience.

View safeguards as integral to a broader financial strategy. This perspective preserves home equity and supports enduring stability.