Flood Risk Assessment Costs $500 But Saves Thousands

Flooding remains one of the most financially damaging and emotionally disruptive challenges for homeowners. As heavy rainfall and unpredictable weather increase, understanding how to fortify a property becomes essential for both safety and financial security. Building climate resilience requires systematic planning, cost analysis, and an informed approach to property maintenance.

Homeowners who treat flood prevention as a structured investment rather than a reactive measure can significantly reduce potential losses and improve long-term property value.

Understanding Flood Risk and Vulnerability

Every property has a unique flood profile influenced by elevation, drainage infrastructure, and surrounding land use. Many homeowners underestimate their exposure because they rely solely on general flood maps or assumptions about distance from rivers. A detailed assessment begins with reviewing contour data, stormwater routes, and municipal drainage capacity.

Even areas outside designated flood zones can experience surface flooding during intense storms. Professional flood risk evaluations often cost between $150 and $500 depending on property size and data complexity. This expense is modest when compared to the potential thousands lost in structural damage or insurance deductibles.

Homeowners should verify whether their local government provides free assessments or mapping tools before hiring private consultants.

The Financial Framework of Flood Prevention

Flood mitigation involves both upfront investments and ongoing maintenance. To make financially sound decisions, categorize expenses into three tiers. Preventive infrastructure costs cover grading, drainage systems, and sump pump installations. Protective barrier costs include flood gates, backflow valves, and water-resistant coatings. Recovery-oriented costs cover insurance premiums, restoration funds, and emergency supplies.

The goal is to balance preventive spending with the probability and severity of potential flooding. For example, installing a backflow prevention valve priced around $300 to $800 can prevent sewage backup that might otherwise result in several thousand dollars in cleanup costs. A clear cost-benefit analysis demonstrates that targeted investments yield measurable financial protection.

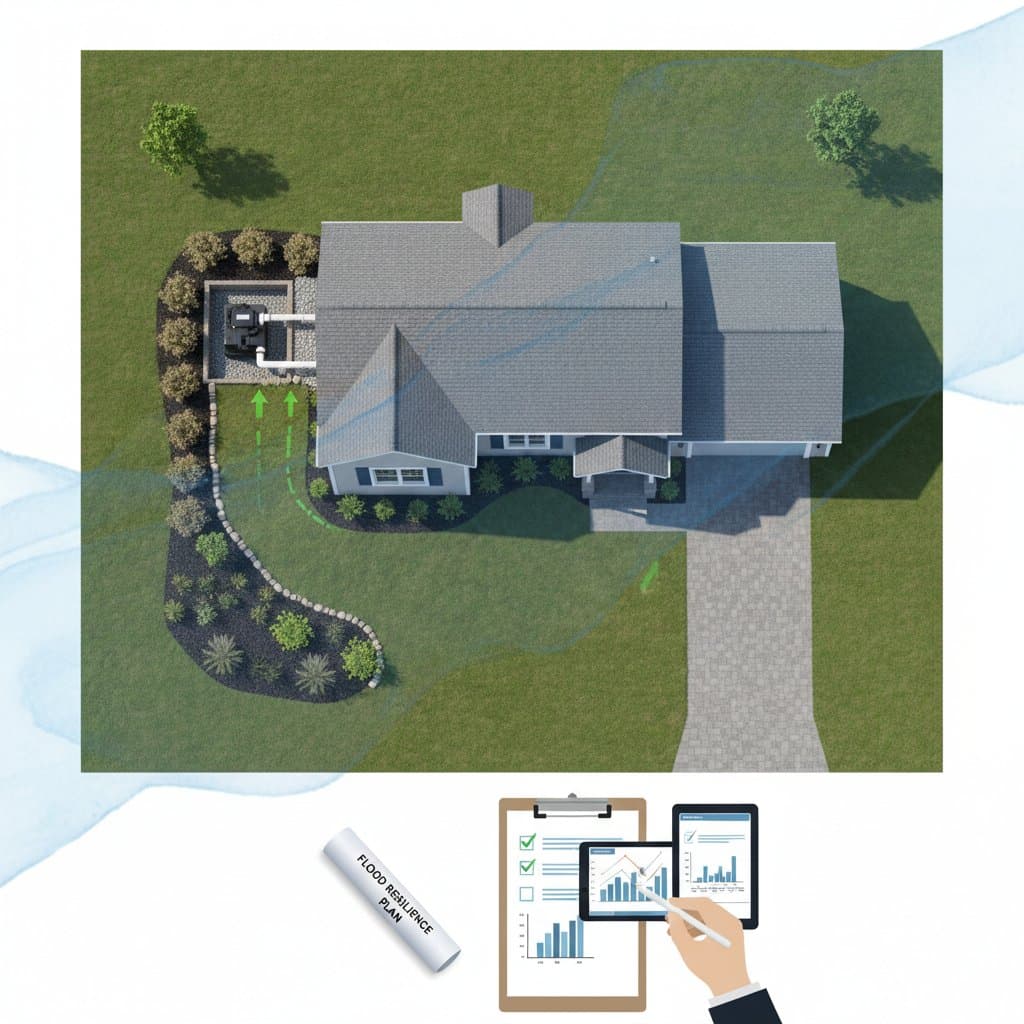

Drainage and Grading Systems

Proper grading ensures water flows away from the foundation instead of pooling near walls. A minimum slope of one inch per foot for at least six feet from the structure is a common standard. Regrading typically costs between $1,000 and $3,000 for an average residential lot.

Although often overlooked, this measure prevents foundation cracks and basement leaks. Installing French drains or surface drainage channels helps redirect runoff during storms. These systems usually involve perforated pipes buried in gravel trenches that collect and transport water to safe discharge points.

Homeowners should verify that discharge locations comply with local regulations to avoid liability for runoff affecting neighboring properties. Routine maintenance is equally critical. Cleaning drain grates, gutters, and downspouts at least twice a year minimizes blockage risks and extends the life of the drainage network.

Sump Pump Systems and Backup Power

A sump pump is the primary line of defense for properties with basements or crawl spaces. It collects water in a pit and automatically pumps it outside once water levels reach a trigger point. Pump units range from $100 to $500, while professional installation can bring the total cost to $1,000 or more.

Homeowners should also budget for a backup power source since power outages often coincide with flooding events. Battery backups cost about $200 to $600 and can operate pumps for several hours. For extended outages, a generator connection provides longer protection.

Regular testing ensures functionality during emergencies. Failing to test the system can lead to silent malfunctions, with devastating results when the next storm arrives.

Flood Barriers and Sealing Techniques

Physical barriers provide temporary or permanent protection at entry points. Removable flood panels, water-activated barriers, and inflatable tubes are common options for ground-level doors and garages. More permanent methods include sealing foundation cracks and applying waterproof coatings on basement walls.

Professional waterproofing averages $3 to $7 per square foot depending on materials used. Homeowners should request written warranties specifying how long the coating or sealant remains effective. Some warranties exclude coverage for hydrostatic pressure, meaning water that forces its way through concrete under pressure.

Reading such fine print prevents misunderstandings about performance guarantees.

The Role of Landscaping in Flood Prevention

Strategic landscaping can control water movement naturally. Swales, rain gardens, and permeable paving materials absorb and redirect runoff. Deep-rooted plants improve soil stability and infiltration capacity.

When designed properly, these features reduce pressure on municipal drainage systems and enhance the property resilience. Landscaping costs vary widely, from $500 for small swales to $5,000 or more for engineered rain gardens with complex drainage layers.

Homeowners should consult both landscape architects and civil engineers before making significant terrain modifications, ensuring that aesthetic choices do not compromise hydrological performance.

Insurance and Financial Protection

Standard homeowners insurance rarely covers flood damage. Separate flood policies fill this gap but can vary greatly in coverage limits and exclusions. Typical premiums range from $400 to $1,200 annually depending on location and structure type.

Deductibles generally start around $1,000, though higher deductibles lower the monthly cost. When evaluating coverage, homeowners should scrutinize replacement versus actual cash value provisions. Replacement coverage reimburses the full cost to rebuild, while actual cash value deducts depreciation.

Policies also differ on whether they cover basements, detached structures, or personal property stored below ground level. Understanding these distinctions prevents costly surprises during claims.

| Coverage Level | Monthly Cost | Service Fee | Coverage Limits | Key Exclusions |

|---|---|---|---|---|

| Basic Plan | $35 to $60 | $0 | Up to $100,000 | Basements, detached garages, landscaping |

| Extended Plan | $60 to $120 | $0 | Up to $250,000 | Coverage limits on luxury flooring, limited personal property |

| Comprehensive Plan | $120 to $200 | $0 | Up to $500,000 | Must meet maintenance requirements, excludes pre-existing damage |

Homeowners should document property conditions annually with photographs and inspection reports. These records strengthen claims and establish maintenance consistency, which many insurers require to honor coverage.

Common Limitations and Claim Denials

Flood insurance and protection plans often contain strict exclusion clauses. Claims may be denied if damage results from groundwater seepage rather than surface flooding. Poor maintenance, such as blocked drains or neglected sump pumps, can also void coverage.

Some policies exclude damage from mold or mildew unless caused by a covered flood event. To minimize denial risks, maintain written logs of maintenance and inspection activities. Keep receipts for all repairs and upgrades related to flood protection.

Insurers often request proof that preventive systems were functional at the time of loss.

Building a Long-Term Resilience Strategy

Flood protection should be integrated into a broader home resilience plan. This includes electrical system elevation, proper insulation materials, and the use of water-resistant flooring in lower levels. Renovation projects provide opportunities to upgrade materials and redesign at-risk spaces.

For example, elevating electrical outlets by at least twelve inches above floor level reduces future repair costs after minor flooding. Homeowners should also evaluate community resilience measures. Participation in local flood mitigation initiatives, such as neighborhood drainage maintenance programs, can yield collective benefits.

Reading the Fine Print Before Service Contracts

Some companies offer flood mitigation service contracts that include annual inspections, maintenance of pumps, and priority emergency response. Before signing, review contract duration, cancellation terms, and scope of coverage. Service fees typically range from $150 to $400 per year.

Protecting Your Investment

Flood resilience is not only about disaster prevention but also about preserving financial stability and property value. Homes equipped with verified drainage systems, sealed foundations, and documented maintenance histories often secure better insurance terms and higher resale prices.

By combining technical upgrades with financial awareness, homeowners can transform flood preparedness from a reactive expense into a strategic investment. Each improvement, from a simple gutter cleaning to a complete grading overhaul, contributes to lasting resilience.